| What on earth is going on? In one of the strangest days of trading oil in history, Brent crude breached $80 per barrel at the first chance to react to the US attack on Iranian nuclear facilities, and then fell. When Iran retaliated by firing missiles at a US military base in Qatar — which might have been expected to send prices upward again — the fall turned into a rout, and Brent dropped below $70. That was a total decline of 13% in response to what appeared to be terrible news. The reason is that the Iranian response has been judged as no more than symbolic. More contentiously, there’s a belief that the issue is over — supported by President Donald Trump’s announcement that Israel and Iran have agreed to a ceasefire to end what he suggested will henceforward be known as the “Twelve-Day War.” Follow here for more developments. Already, Trump’s reaction to a direct attack on a US base had showed that he saw it exactly as the oil market did. Stating that no Americans had been harmed, he said: Most importantly, they’ve gotten it all out of their “system,” and there will, hopefully, be no further HATE. I want to thank Iran for giving us early notice, which made it possible for no lives to be lost, and nobody to be injured. Perhaps Iran can now proceed to Peace and Harmony in the Region, and I will enthusiastically encourage Israel to do the same.

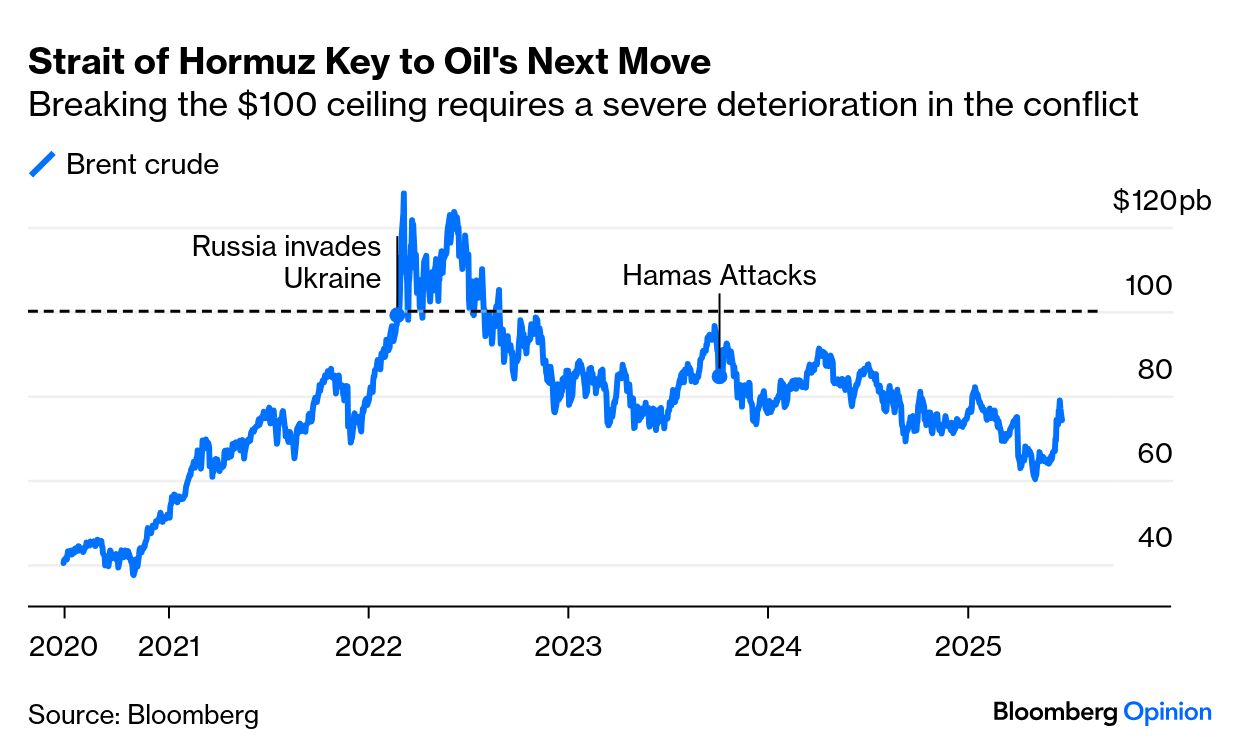

If the Iranian attack was meant to help the regime save face at home, this response almost completely invalidated it. Drawing such praise from a US president scarcely saves Tehran’s honor, and it’s hard to believe that it’s “all out of their system.” Are the reactions premature? And how can a chapter of hostilities including what is effectively the long-feared “big one” have been received so differently from the last serious geopolitical shock, when Russia invaded Ukraine in 2022? That episode took Brent to $120: Robin Brooks of the Brookings Institution explains why exploding the most powerful bomb to be used in conflict since Nagasaki has had comparatively little impact: The risk of Russian oil supply being taken off the global market was high, at least in markets’ eyes during those early weeks following the invasion. The sad truth is that the same does not hold true for the Middle East. Markets are inured to endless violence, which means that the hurdle for severe market fallout is higher.

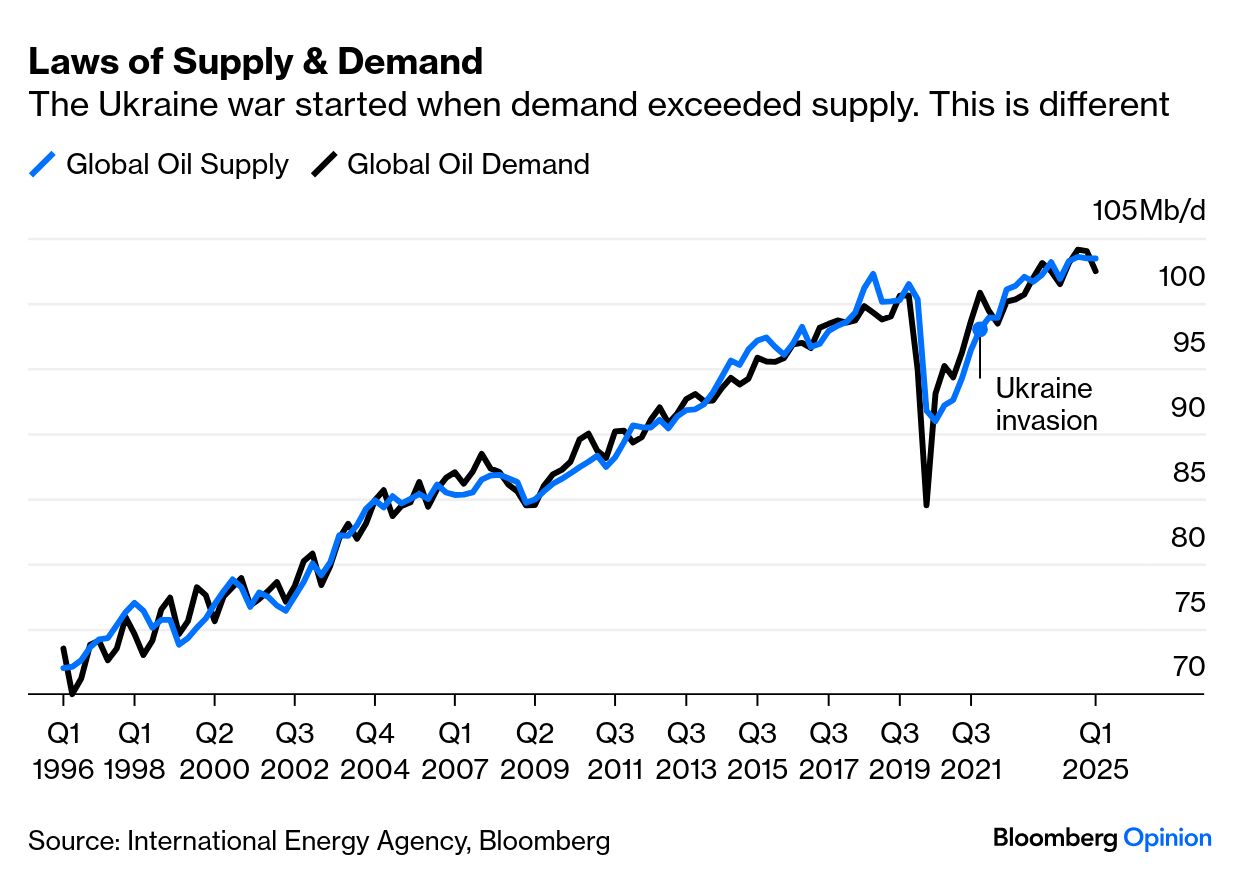

A missile strike against a military target — rather than hitting energy infrastructure in a way that damaged the supply of oil — can in this context be seen as good news. There’s also the fact that the dynamics of supply and demand were pushing the oil price upward three years ago, whereas now supply exceeds demand. This is how global oil demand compares to output in the last three decades, according to the International Energy Agency: So far in this conflict, oil has only briefly topped $80 per barrel, then retreated. The market consensus was that Iran’s next move would be telling. The missiles fired at Qatar, though not a definitive olive branch, was more or less the best-case scenario. With more than a fifth of the world’s oil production transiting the Iran-controlled Strait of Hormuz, the regime retains high leverage on where oil prices head next. A closure would have far-reaching consequences. It’s not yet clear, despite the market reaction, that Iran’s muted initial response means that this option is off the table. However, there are strong inducements not to close the Strait. Ted Gardner of Westwood’s Enhanced Midstream Income ETF argues that a blockade would most hurt Iran’s allies, particularly Iraq and China. Further, the regime still has much to lose even after the US attacked its nuclear program: The fact that Trump and Israel haven’t targeted Iran’s economic infrastructure — only military and nuclear — means Iran hasn’t lost much beyond nuclear capability. If their economic infrastructure were hit, we’d be far more likely to see retaliation through a Strait closure.

Against this, there is still the argument that disruption to the Strait of Hormuz could in a worst-case scenario drive prices above $130 per barrel. Capital Economics’ David Oxley, who made this forecast, argues that the countries that would be most affected happen to hold nearly 95% of OPEC+’s 5.5 million barrels per day of spare capacity: As well as disrupting the flow of energy to the global market, a closure of the Strait would also severely limit the extent to which OPEC+ could employ its spare capacity to offset upward pressure on oil prices.

A further question is whether higher prices would be sustained. The longer they’d last, the greater the risk of pass-through to consumer prices and, subsequently, central banks’ rate decisions. Seth Carpenter, Morgan Stanley’s chief global economist, notes that oil never returned to its $82 peak from mid-January. Since then, as Points of Return reported here, more central banks have cut than hiked. “History suggests that a 10% permanent increase in oil prices moves core inflation by only a couple of basis points,” says Carpenter, “an amount that easily gets lost in the noise.” Moreover, the US is the world’s largest oil producer. The European Union’s exposure to Middle East disruption also appears minimal. The Complexity Science Hub (CSH) and the Supply Chain Intelligence Institute Austria’s analysis of six years of vessel-tracking data found that only around 10% of tanker trade through the Strait is destined for the EU — translating to just 4% of the EU’s total tanker imports. Nevertheless, CSH found that the UAE alone accounts for 20% of global aluminum exports — dependent on bulk shipping through the Strait. Alternative routes for oil via pipelines in Saudi Arabia are already near capacity and increasingly vulnerable to attacks by Iran’s Houthi proxies. Tehran’s limited retaliation will likely continue to ease the pressure on prices — but only if this is truly the end of the matter. High inventories and weak demand have weakened Iran’s leverage, but not removed it altogether. Monday’s drastic price fall brought oil to a position where the risks to the upside appear to exceed those to the downside. As Trump is fond of saying, we’ll see. —Richard Abbey |