The Week in Breakingviews |

| |

|

The Week in Breakingviews |

| |

|

Insights from Reuters global financial commentary team |

|

|

By Peter Thal Larsen, Global Editor |

|

|

Welcome back! The U.S. Supreme Court has struck down President Donald Trump’s emergency tariffs. Does this mean the global trade war is over? Let us know what you think. If this newsletter was forwarded to you, sign up here to get it in your inbox every weekend.

Note: Links in this newsletter require a Breakingviews subscription. To sign up for a free trial, click here. |

|

|

“‘The falcon cannot hear the falconer,’ William Butler Yeats wrote at the beginning of ‘The Second Coming’. In the turbulent world of private credit, it seems Blue Owl can no longer hear the owler.”

Read more: Blue Owl picks private credit’s path of pain. |

|

|

Five things I learned from Breakingviews this week |

-

Big Tech firms could collectively borrow up to $700 billion more without suffering a credit rating downgrade.

- Stablecoin giant Tether’s cash buffer is just 3.3% of the $184 billion coins in circulation.

- Indian retail investors’ derivatives losses increased 41% in the last financial year.

-

Hungarian Prime Minister Viktor Orbán has met with three French presidents, three German chancellors, and eight Italian prime ministers since 2010.

- Russia’s finance minister has suggested legalising online casinos.

|

|

|

A boardroom is seen in an office building in Manhattan, New York City, New York, U.S., May 24, 2021. REUTERS/Andrew Kelly |

There was a time when activist investors caused panic in corporate boardrooms. The arrival of a cage-rattling shareholder meant heightened media scrutiny, bruising public criticism, and the threat that executive heads would roll. Memorable campaigns such as TCI’s push to break up Dutch lender ABN Amro, Bill Ackman and Carl Icahn’s wrestling match over Herbalife, and Nelson Peltz’s crusade to join the board of Procter & Gamble persuaded company directors that activists were to be feared – and ideally avoided.

Activists are no less active today. In just the past few weeks Jana Partners has pushed for a breakup of financial technology firm Fiserv, Dan Loeb waded into a takeover involving Spanish defence contractor Indra Sistemas, and Elliott Management took a stake in British data provider LSEG and was reported to have snapped up a chunk of Norwegian Cruise Line. Elliott’s intervention also forced Japanese car giant Toyota Motor to delay a plan to buy out an industrial affiliate, while $17 billion Genuine Parts announced a split after Paul Singer’s firm pushed for a boardroom overhaul last year.

Despite all this activity, activists are less aggressive than before. That’s partly because companies have become more skilled at dealing with uppity investors. Where executives used to wave away unwanted shareholders, they now engage in dialogue. Specialised advisers at firms like Lazard and Jefferies help companies craft plans to deal with activist campaigns. Some groups, like UBS shareholder Cevian Capital, aim for constructive criticism.

|

|

|

Who benefits from all this agitation? Perhaps surprisingly, the activists’ own investors are not obvious winners. As Sebastian Pellejero points out, activist hedge funds have returned a healthy annual 12%, after fees, since 2022. But over the past decade that return drops to just over 6% a year – much less than the reward investors got from simply tracking the S&P 500 benchmark. Like the broader universe of active fund managers, it seems that activists underperform the index.

Another supposed benefit of activists is that they make capital markets work more efficiently by keeping tabs on incompetent or lazy management teams. Yet here too the evidence is far from conclusive. In aggregate, companies that reached truces with boardroom agitators underperformed the S&P 500 by 7% over the next three years. Activists may be on the up, but their advantages are far from apparent. |

|

|

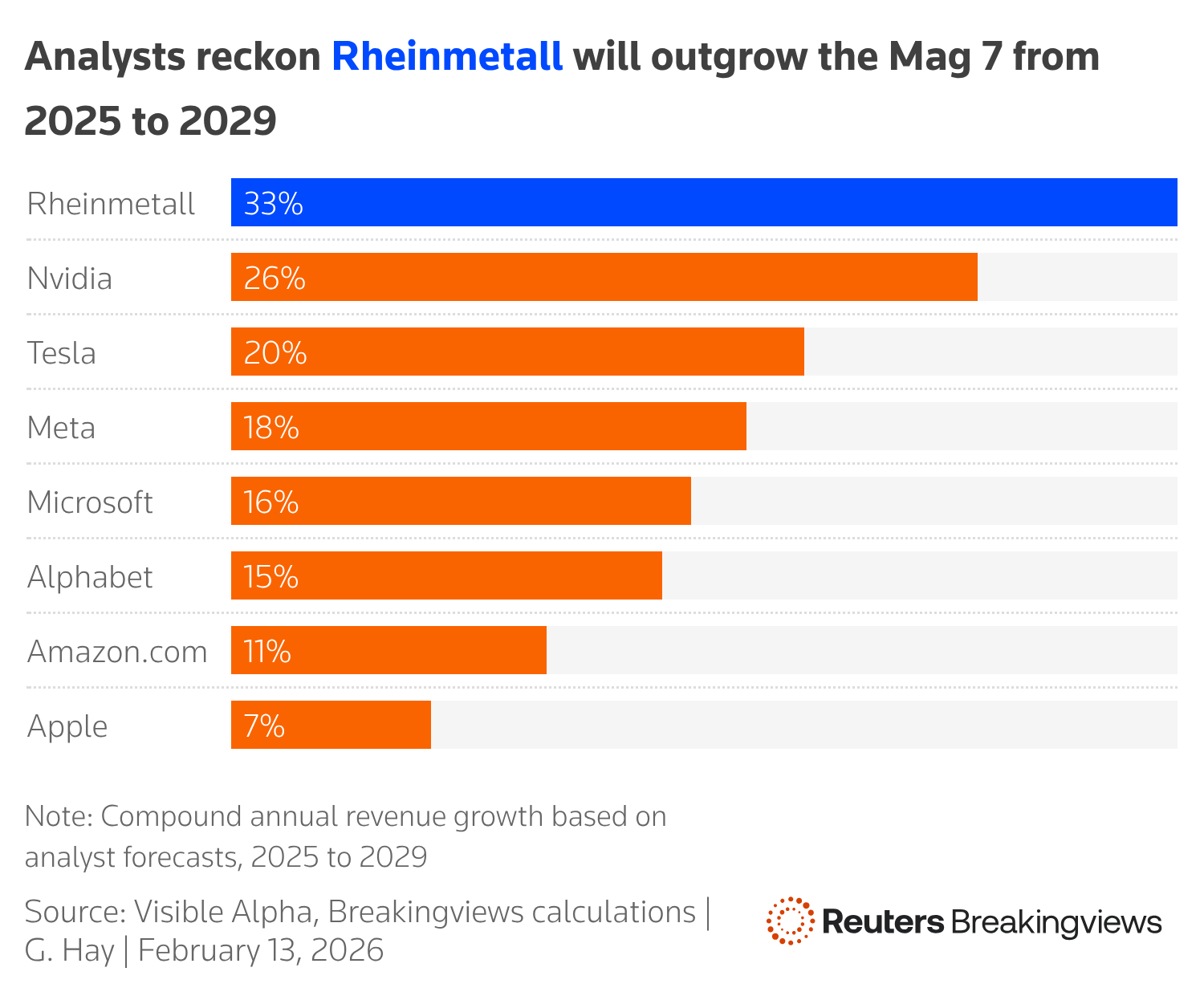

Rheinmetall is the poster child for European rearmament. The German tankmaker’s market value has soared from 4 billion euros four years ago to 70 billion euros today. Its ability to snag a large share of Europe’s increased defence spending means analysts expect its revenue to grow faster than the “Magnificent 7” big technology companies. Is this good for competition? George Hay has his doubts.

|

|

|

Stock market investors may be in two minds about the artificial intelligence boom, but big tech firms are still cranking up spending: they’re due to invest roughly $700 billion this year. On The Big View this week I talked to Andrew Sheets, Morgan Stanley’s head of fixed income research, about what the splurge means for debt investors, and how governments and central banks around the world are helping to support markets.

The Munich Security Conference has become the must-attend event where defence experts, politicians, policy wonks and financiers rub shoulders. On the Viewsroom this week George Hay – just back from the Bavarian capital – and Pierre Briancon debated the challenges of Europe’s defence spending splurge with Aimee Donnellan and Jonathan Guilford. |

|

|

Vaccines are a miracle of modern medical science. Widespread inoculations against diseases like measles, polio and smallpox have transformed human health, while the Covid vaccine reminded us all of the awesome power of a simple jab. Yet the business is looking sickly. As Aimee Donnellan |

|

|

|